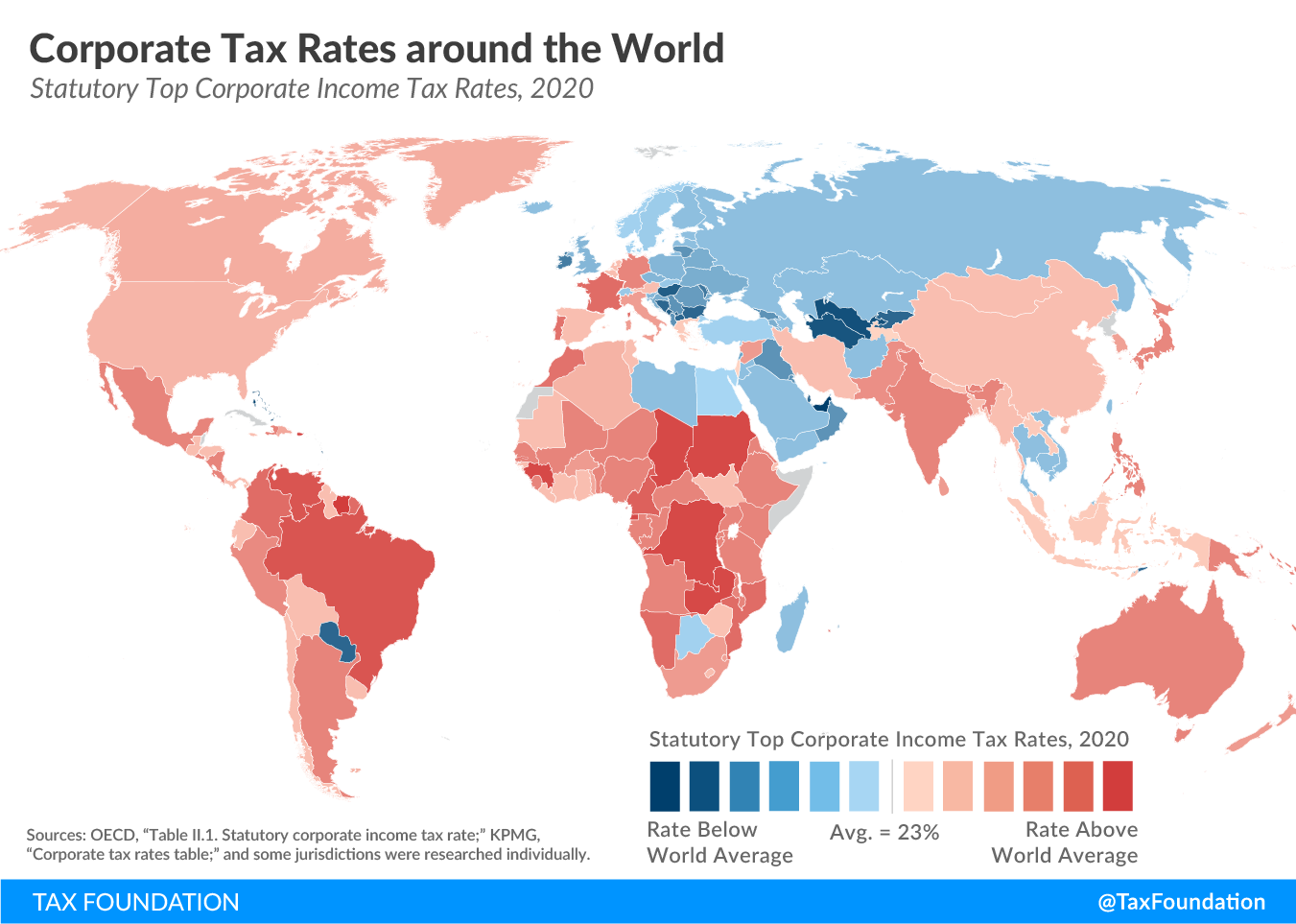

Corporate tax rates play a pivotal role in shaping economic policy, influencing everything from business investments to wage growth impacts. The debate surrounding these rates has intensified, especially in the wake of the 2017 Tax Cuts and Jobs Act, which drastically reduced the corporate income tax rate from 35% to 21%. Harvard economist Gabriel Chodorow-Reich has been at the forefront of analyzing the aftermath of this legislation, raising important questions in the ongoing tax policy debate. As key provisions of the TCJA are set to expire, figures like Kamala Harris advocate for increased corporate tax rates to fund essential social programs, while Donald Trump argues for sustaining lower rates to encourage economic expansion. This discourse not only reflects partisan divides but also the complexities of tax administration in a dramatically evolving global economy, where the effects of such policy shifts demand careful reevaluation and understanding.

When discussing corporate taxation, it’s essential to consider terms like business tax obligations, statutory rates, and fiscal policy relating to corporations. The legislative reforms initiated by the 2017 Tax Cuts and Jobs Act ushered in a significant transformation in the corporate tax landscape, leading to a greater focus on the implications of tax policy on corporate decision-making and investment behavior. Major economic figures, including Gabriel Chodorow-Reich, have explored how shifts in these fiscal frameworks can impact business profitability and consequently influence wage structures within the labor market. With the expiration of critical provisions approaching, the dialogue regarding the adjustment of corporate tax obligations is more relevant than ever. As policymakers grapple with potential reforms, understanding the multifaceted effects of tax legislation is crucial to fostering a balanced economic environment.

Impact of the 2017 Tax Cuts on Corporate Tax Rates

The 2017 Tax Cuts and Jobs Act (TCJA) saw a significant restructuring of corporate taxation in the United States. By slashing the corporate tax rate from 35% to 21%, the TCJA aimed to stimulate economic growth and boost wages through increased investments. Economist Gabriel Chodorow-Reich, along with his co-authors, explored the impact of these cuts in their study published in the Journal of Economic Perspectives, revealing a complex relationship between tax rates and real economic outcomes. While some firms did boost their investments post-TCJA, the substantial drop in tax revenue raised questions about the sustainability of budget balances in the long-term economy, fueling a robust tax policy debate in the years that followed.

The analysis brought to light several compelling observations regarding the corporate income tax under the TCJA. Although proponents argued that lowering corporate rates would lead to a surge in business reinvestment, Chodorow-Reich’s findings suggest that the modest increases experienced in wage growth and investments did not compensate for the dramatic decrease in tax revenues. As these tax cuts are now set to expire by 2025, lawmakers are faced with the difficult task of deciding whether to reinstate the former rates or consider alternate reform measures. This continuing discourse reflects the need for mindful tax reform that balances growth incentives with fiscal responsibility.

Debate Over Corporate Income Tax Policy

The corporate income tax policy in the U.S. has become a contentious issue among policymakers, especially as the expiration of the TCJA looms closer. The tax policy debate exposes significant divisions between the two major parties, with Democrats like Kamala Harris advocating for an increase in corporate rates to fund social programs while Republicans, including Donald Trump, push for further cuts to stimulate economic growth. This polarization illustrates the varying economic philosophies held by different factions and highlights how tax laws can influence both business strategies and consumer welfare. Chodorow-Reich’s research adds depth to this narrative by providing empirical evidence that informs the discussion surrounding corporate tax rates.

Moreover, the retrospective examination of the TCJA’s impacts underscores an essential question: how do changes in corporate income tax policy affect broader economic metrics such as wage growth? As the debate progresses toward the next election cycle, understanding the tangible outcomes of past tax reforms becomes critical. With studies indicating that the expected $4,000 wage increase per employee did not materialize as predicted, Chodorow-Reich invites both sides to reconsider their positions on corporate taxation. Essentially, the outcomes of these tax policies will reverberate long past 2025 and will likely shape the prevailing narratives around economic growth in future congressional discussions.

Wage Growth Impacts of Corporate Tax Reform

One of the pivotal discussions around the TCJA is its impact on wage growth, and how corporate tax reductions directly correlate to the paychecks of American workers. Proponents of tax cuts often claim that lower rates for businesses lead to higher investment in labor and subsequently drive wage increases. However, Gabriel Chodorow-Reich’s findings suggest a more tempered reality, where the actual increases in wages amounted to an average of only $750 per year for full-time employees, significantly less than initial projections that ranged as high as $9,000. Such disparities indicate that while corporate tax reforms are intended to benefit workers, the expected outcomes may not align with reality.

This wage growth discussion becomes even more critical in light of the varying economic contexts since the implementation of the TCJA. For instance, factors such as inflation and fluctuations in corporate profitability during the pandemic have influenced labor demands and wage structures. Chodorow-Reich emphasizes that a nuanced understanding of these dynamics is crucial for future tax policies. If lawmakers aim to stimulate wage growth, targeting specific provisions, such as expensing strategies that directly link to workforce expansion, may prove more effective than simply adjusting corporate tax rates. Thus, wage outcomes from tax reform are complex and require careful consideration of broader economic indicators.

Future of Corporate Tax Revenue in the U.S.

As the expiration of key provisions from the 2017 Tax Cuts and Jobs Act approaches, the future of corporate tax revenue is shrouded in uncertainty. Following the initial plunge of 40% in revenues post-TCJA, some recovery was observed beginning in 2020, coinciding with increased business profits during the pandemic. Chodorow-Reich’s analysis points toward the potential for tax revenues to rebound as corporate profits exceed expectations, yet this recovery invites scrutiny over the long-term sustainability of such profits under low taxation. What remains clear is that fluctuations in corporate earnings will significantly influence discussions on tax policy moving forward, particularly in an election year.

The implications of the TCJA’s expiration present a crucial juncture for policymakers as they weigh alternatives that could replace or reform existing laws. One option suggested by economists is to raise corporate statutory rates while restoring favorable provisions like immediate expensing for capital investments. This dual approach could potentially generate necessary revenue while simultaneously encouraging businesses to invest in growth. As lawmakers navigate this challenging terrain, a careful analysis of past tax reforms will provide valuable insights into forging a more balanced and effective tax policy that meets both economic and social objectives.

Examining the Effects of the TCJA on Investment

The TCJA aimed to promote investment in U.S. businesses through substantial tax cuts and incentives, but the actual effects have generated significant debate. Chodorow-Reich and his colleagues found that while capital investments rose by about 11% in the aftermath of the law, the benefits were unevenly distributed. The analysis highlighted that contrary to the blanket assertion that tax cuts universally spur business investment, specific provision expirations saw highly targeted and more effective capital investments than traditional rate reductions. This raises important questions about the design of tax incentives and whether they should be tailored to incentivize particular behaviors within the business landscape.

The discrepancies in investment responses suggest that merely lowering corporate tax rates does not guarantee a stimulated economy. Instead, it may be more prudent for future reforms to focus on individualized provisions that drive strategic investment decisions—such as increased capital investment allowances and research and development credits. In considering the effectiveness of tax policies, it is crucial for lawmakers to avoid a one-size-fits-all mentality and instead foster a dialogue surrounding evidence-based reforms that align with contemporary economic realities and international competition.

The Role of LSI in Corporate Tax Discussions

As tax policy continues to evolve amid shifting economic landscapes, the integration of Latent Semantic Indexing (LSI) emerges as a valuable tool in facilitating nuanced discussions regarding corporate tax reform. By understanding the semantic relationships between various terms—such as the effects of the 2017 Tax Cuts and Jobs Act, impacts on wage growth, and the intricacies of corporate income tax—policymakers can forge a deeper connection to how changes in tax policy resonate with constituents. This analytical framework enhances communication strategies, ensuring a clearer articulation of economic principles and the potential outcomes of differing tax strategies.

Leveraging LSI can also pave the way for more informed debates on corporate taxation, inviting diverse perspectives to engage with the intricacies of tax policy. With terms like ‘wage growth impacts’ and ‘tax policy debate,’ approaching fiscal discussions through lenses of connectivity can help bridge divides among stakeholders, enabling collaborative efforts to design equitable and efficient taxation laws. As we approach the pivotal decisions surrounding the TCJA’s expiration, employing LSI will be essential in fostering conversations that transcend partisan lines and focus on achieving sustainable economic progress.

Corporate Tax Revenue Trends Post-TCJA

The trends surrounding corporate tax revenue following the passage of the TCJA illustrate a compelling narrative of volatility and recovery. Initially, the law caused a dramatic drop in tax revenue, but as the economy began to rebound in 2020, revenue from corporate taxes surged beyond original estimates. Analysts like Chodorow-Reich examine the reasons behind this trend, pointing to an unexpected spike in corporate profitability that was not universally anticipated amidst a global recession. As businesses adapted to new market conditions during the pandemic, their financial performances improved, leading to an unforeseen resurgence in corporate tax contributions.

These changes prompt a reevaluation of the assumptions surrounding corporate taxation and the effects of legislative reforms. The resurgence of corporate revenue positions lawmakers to reconsider the potential benefits of lowering rates, as it challenges the assertion that high rates yield diminished returns. As we approach the renewal of key tax provisions, it is imperative to align tax policy with empirical evidence, ensuring that any adjustments made foster not only corporate interests but also equitable economic growth for the broader population.

Lessons Learned from the TCJA Implementation

The implementation of the 2017 Tax Cuts and Jobs Act offers critical lessons as policymakers reflect on its outcomes. One significant takeaway from Gabriel Chodorow-Reich’s analysis is the disparity between projected and actual economic benefits stemming from corporate tax cuts. While the aim was to stimulate growth and bolster wages, the findings highlighted a more complex reality, where significant revenue losses were reported alongside only modest increases in business investment and wage growth. Such outcomes serve as a cautionary tale for future tax reforms, emphasizing the necessity for thorough analyses and realistic expectations regarding the consequences of tax legislation.

Second, the discussions emerging from the TCJA’s provisions signify the importance of data-driven decision-making in shaping tax policy. As lawmakers gear up for the next legislative session, the lessons learned underscore the need for a comprehensive understanding of how corporate tax rates influence not only business behavior but also the overarching economic landscape. To navigate the future effectively, it will be essential to develop tax strategies that are both proactive and responsive to current market demands, ensuring that all stakeholders benefit from a streamlined and equitable taxation environment.

Frequently Asked Questions

What are the current corporate tax rates in the U.S. and how do they compare to those established by the 2017 Tax Cuts and Jobs Act?

As of now, the U.S. corporate tax rate stands at 21%, a reduction from the previous 35% set before the 2017 Tax Cuts and Jobs Act (TCJA). This significant cut was designed to stimulate economic growth by encouraging business investments and was the centerpiece of tax policy changes debated in the years following its enactment.

How did the corporate tax cuts from the 2017 Tax Cuts and Jobs Act affect corporate income tax revenue?

The corporate tax cuts introduced by the TCJA led to an immediate 40% drop in corporate tax revenue after its implementation. However, corporate tax revenues began to rebound starting in 2020 as business profits exceeded expectations, illustrating a complex relationship between corporate tax rates and income tax revenues.

What impacts on wage growth have been observed since the corporate tax rate cuts of the 2017 Tax Cuts and Jobs Act?

Following the enactment of the TCJA, wage growth has seen modest increases. While some estimates predicted significant wage hikes of up to $9,000 annually, actual figures indicated a more modest increase of around $750 per year. This discrepancy highlights ongoing debates about the effectiveness of corporate tax cuts concerning wage growth.

What are the key provisions of the 2017 Tax Cuts and Jobs Act that affected corporate investment?

The TCJA included provisions that allowed companies to immediately deduct the full cost of new capital investments, which was aimed at encouraging business spending. This policy contributed to an approximate 11% increase in corporate investments post-TCJA, though it also raised questions about the effectiveness of straight corporate tax rate cuts.

How are ongoing debates regarding corporate tax rates linked to the 2017 Tax Cuts and Jobs Act?

Debates around corporate tax rates have become a significant part of the political discourse, with some arguing for increases to fund social initiatives while others advocate for lower rates to enhance business growth. The analysis by economists like Gabriel Chodorow-Reich provides evidence that these rates have profound implications for investment and wage growth, making them crucial in the tax policy debate.

What role did Gabriel Chodorow-Reich play in analyzing the impacts of corporate tax rates from the TCJA?

Gabriel Chodorow-Reich, a macroeconomist at Harvard, co-authored an analysis assessing the real-world impacts of the corporate tax cuts from the TCJA. His research revealed discrepancies between expectations of economic growth from tax cuts and actual outcomes, providing critical insights into the relationship between corporate tax policy and its ramifications on investment and wages.

Is there bipartisan consensus on the effects of corporate tax cuts enacted by the 2017 Tax Cuts and Jobs Act?

While there is some bipartisan acknowledgment of the need for tax reform, opinions remain divided on the effectiveness of the corporate tax cuts established by the TCJA. Supporters argue these cuts fuel investment, while critics cite insufficient benefits in wage growth and revenue generation, reflecting the ongoing complexities in the tax policy debate.

| Key Points |

|---|

| Congress is preparing for a tax battle in 2025, as key provisions of the 2017 Tax Cuts and Jobs Act (TCJA) are set to expire. |

| The TCJA reduced corporate tax rates from 35% to 21%, impacting tax revenue significantly. |

| Economic analyses show that the tax cuts led to modest increases in wages and business investments, but tax revenue dropped substantially. |

| Different political perspectives exist: some advocate for raising corporate tax rates to fund initiatives, while others argue for further cuts to stimulate the economy. |

| The analysis concluded that capital investments increased under the TCJA, particularly due to provisions allowing immediate write-offs for new investments. |

| Corporate tax revenue decreased by 40% initially but began recovering in 2020, driven by higher than expected business profits. |

| Public debate continues over the effectiveness of corporate tax cuts on investment and wage growth, with varying interpretations of the outcomes. |

Summary

Corporate tax rates are a contentious issue as Congress approaches critical legislative changes in 2025. The expiration of several provisions from the 2017 Tax Cuts and Jobs Act (TCJA) has reignited debates on the merits of raising or lowering corporate tax rates. The analysis by economist Gabriel Chodorow-Reich highlights the complexity of the impact these tax policies have had on both revenue and business investments. Understanding corporate tax rates is essential for shaping economic policies that can effectively stimulate growth while ensuring sufficient government revenue.